When I used Claude to build a US Large Cap Resilience Index recently, something jumped out at me. Something I haven’t seen much in-depth research on.

I have seen a lot of coverage of the resource intensity of data centres powering AI – the intense demand for energy and water And rightly so; these data centres require massive resources and that can put strain on existing infrastructure.

But when I mapped the operational exposure of US companies, I was able to look at that relationship in reverse. The extent to which the environment creates risk for critical AI infrastructure.

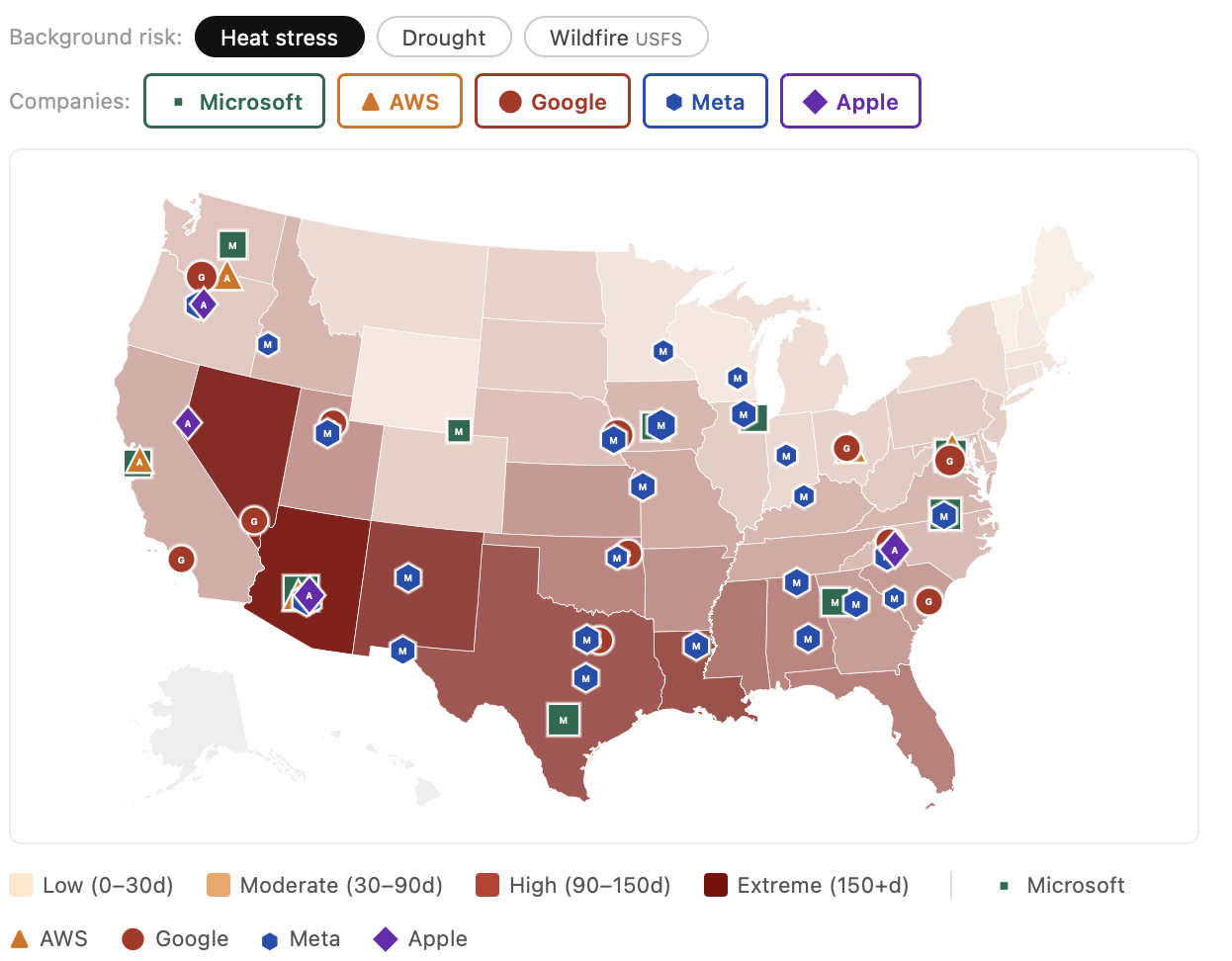

This week I went deeper to map this more comprehensively including building an interactive investor map of the major extreme weather risks facing major hyperscalers through their data centre footprints.

TLDR: Hyperscalers have key data centre assets concentrated it in some of the most physically climate-stressed locations in the US. Phoenix, Texas and even the Pacific Northwest already face dangerous heat, wildfires, water stress, and/or a structurally weakening grid, and the AI buildout is amplifying every one of these pressures. Opacity of information and a lack of market awareness mean these risks are not being priced.

Changing Asset Intensity Heightens Climate Risk

Tech as a sector generally scores highly on climate resilience because of the traditionally asset light nature of these firms. But that story is changing in the race for compute.

Microsoft, Alphabet, Amazon, and Meta are collectively expected to invest up to $725 billion in AI infrastructure in 2026. Their heavier asset footprint weighed on their initial scores when Claude and I built the Resilience Index but these scores were only based on a sample of data centre operations.

To dig deeper, I used Claude to try to identify a more thorough picture of data centre exposures for these hypserscalers. I overlaid climate risk maps from Probably Futures and US Wildfire Risk with publically disclosed data centre locations for the big hyperscalers.

This is where the first investor risk became apparent: opacity in data centre locations.

For strategic reasons, tech firms do not always declare their full data centre footprint. Often they will indicate regional exposure where they have multiple buildings as opposed to address specifics.

Looking at the major names in this exercise, we were able to gather the following data centre data from public sources:

- Meta –The 24 markers represent every Meta-owned US data centre campus disclosed on their official site.

- Alphabet (Commonly referred to as Google) — 9 named US cloud regions plus 2 additional physical locations, covering the full publicly disclosed compute geography.

- Microsoft — All 10 named US public Azure commercial regions representing clusters of multiple buildings within that metro area.

- Amazon (AWS) — All 4 named US commercial regions plus one known additional physical presence (Phoenix). Same caveat: each region contains multiple data centre buildings.

- Apple — 4 known US owned locations are shown. Apple discloses the least of the group and leased colocation capacity is unknown but likely to exist.

Mapping Hyperscaler Data Centre Exposure in the US

Below you’ll find an interactive map highlightingg the data centre locations of these major tech names overlaid with key climate risks: heat stress, drought and wildfire.

It is important to remember that these extreme weather risks have direct implications for data centres:

- Heat stress: Data centres generate massive heat that needs to be removed continuously.

- In extreme heat, cooling systems lose efficiency, water consumption spikes, equipment degrades faster, and the grid weakens — all at once — which is why heatwaves have already forced data centre shutdowns at Google, Oracle and X facilities.

- Drought: Data centres consume enormous volumes of water for cooling — a single hyperscale facility can use millions of gallons a day and rising as AI demand rises.

- Droughts put data centres in direct competition with agriculture and residents for a shrinking resource, creating both regulatory risk (water-use restrictions, permit denials, community opposition) and operational risk (forced curtailment of cooling capacity precisely when heat is highest).

- Wildfires: Wildfire smoke and ash clog the air filtration and evaporative cooling systems data centres rely on, and can force temporary shutdowns even when the facility itself isn’t in the fire’s path.

- California, Oregon and Arizona facilities have all faced this in recent years.

- Beyond direct site risk, wildfires also damage the transmission infrastructure that supplies power to data centres, with utilities increasingly imposing public safety power shutoffs that interrupt service across entire regions during peak fire conditions.

Looking at these maps, a few geographic hotspots jump out:

The High Risk Concentration: Phoenix, Arizona

This is one of the fastest-growing AI data centre locations in the US precisely because of cheap land and power. Microsoft, AWS, Apple and Meta all operate in the Phoenix metro.

However, Phoenix faces approx.161 days above 35°C today, rising to 166 at 2.0°C, with severe water stress compounding the heat. The water intensity of data centres makes this a risk hotspot in more ways than one.

The Underestimated Risk: Pacific Northwest

Four hyperscalers built data centres in Oregon — Alphabet in The Dalles, Meta and Apple both in Prineville, and AWS in Boardman. The assumption was that the Pacific Northwest offers cool temperatures, cheap hydropower, and water security.

While the map correctly shows moderate average risks for the region, there are important risks not being captured. At 2.0°C, the region faces increasing wildfire smoke disruption, precipitation regime change that puts long-run water availability in question and tail heat risks – all of which the map cannot show. This is an important limitation of state mapped average climate risk analysis that we need to be honest about.

Northwest hydro generation, which has already fallen in recent years, is set for further challenge as glacier melt and snowpack declines challenge the ‘cheap, abundant hydro’ thesis for these data centres.

Even more worryingly, the Dalles, where Google’s data centres sit, faces extreme and exceptional drought according to the US drought monitor but Alphabet refuses to disclose water use under the justification of trade secrets. This is often used by data centre operators but it means our capacity to even understand how they’re managing water risks is extremely limited.

Where Climate Risk meets Grid Weakness: Texas

Microsoft, Alphabet, Meta and Amazon all have material Texas exposure through their data centre locations.

Three different risks compound in these locations:

- First, the heat itself — most Texas locations score 110–175 days above 35°C.

- Second, the grid is structurally fragile to both extreme cold and extreme heat, with energy regulators warning explicitly about AI-driven load growth.

- Third, water stress is high across the state, with drought scores between 42% and 55% likelihood of a multi-year drought.

The Investment Opportunity: Adaptation Solutions

While the risks in these locations are formidable, the importance of these data centres to the next leg of economic growth means solutions will be sought and found.

The reality is that these companies need to find solutions to manage data centres in these extreme conditions — and fast. That necessity combined with the economic might of these companies will create winners in the form of adaptation solution providers.

Investors who understand these risks are best positioned to identify these technologies and benefit from their growth trajectories – something I’ll cover in a future edition of the Resilient Investor. I will also look at resilience in hyperscaler locations outside the United States.

If you’d like to follow along, please subscribe using the button below and email [email protected] with any questions.